Asian Gaming Markets Guide

Asia Pacific represents the world's largest and most complex gaming ecosystem, commanding 52.3% of global gaming revenue and home to over 1.5 billion gamers across vastly different markets. With the region generating $155.25 billion in 2024 and projected to reach $281.5 billion by 2030, understanding the nuances between Asian markets has become essential for any gaming company with global ambitions.

Yet Asia defies simple categorization. While Western companies often treat it as a monolithic opportunity, the reality encompasses everything from China's tightly regulated $45 billion market to Southeast Asia's mobile-first $5.89 billion ecosystem, from Japan's console gaming heritage to India's explosive mobile growth. Each market operates under different regulatory frameworks, cultural preferences, monetization models, and competitive dynamics that require distinct strategic approaches.

Having worked across these markets for over a decade, I've witnessed how seemingly similar countries can have fundamentally different gaming ecosystems. Success requires moving beyond demographic similarities to understand the regulatory complexities, cultural nuances, and technological infrastructure that define each market's unique opportunity and challenges.

Market Size and Regional Overview

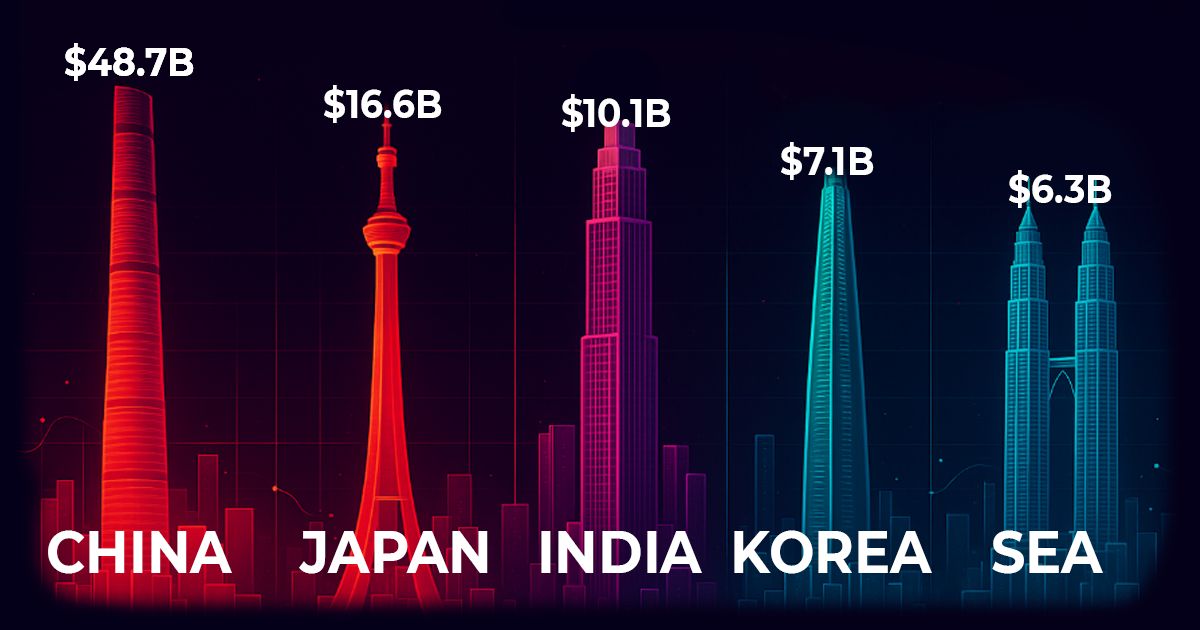

The sheer scale of Asia Pacific gaming dwarfs other regions, but the distribution reveals fascinating patterns that shape market entry strategies. China dominates with approximately $45 billion in revenue, representing nearly 30% of the global market, while Japan contributes $6.19 billion despite its smaller population. Korea generates significant revenue relative to its size, and India's $4.04 billion market is growing at the fastest rate in the region.

Southeast Asia's six major markets—Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam—collectively represent $5.89 billion in 2024, with projections reaching $7.37 billion by 2027. Australia and New Zealand contribute $2.5 billion and $419.84 million respectively, representing mature Western-style markets within the Asian ecosystem.

Mobile gaming represents 42.5% of regional revenue, but this percentage varies dramatically by market. While mobile dominates in Southeast Asia at over 70% of revenue, Japan and Korea maintain significant console and PC gaming segments. Understanding these platform preferences is crucial for product development and marketing allocation decisions.

China: The Regulated Giant

China's gaming market operates under the world's most sophisticated regulatory framework, where every game requires approval from the National Press and Publication Administration (NPPA) before launch. With 850 million netizens and 783 million smartphone users, the market potential is massive, but the regulatory complexity creates significant barriers for international companies.

The regulatory landscape has evolved significantly since 2018, when the NPPA assumed full control over gaming oversight. In 2024, the average of 106 gaming licenses per month represents a more stable environment compared to the approval freezes of 2021-2022. However, foreign games face additional scrutiny, with only 75 imported games receiving approval in 2024 compared to over 1,200 domestic titles.

Content restrictions go beyond violence and sexuality to include cultural and political sensitivities. Games featuring imperial themes, excessive individualism, or content deemed contrary to Chinese values face rejection. The December 2023 draft regulations, which were quickly walked back after causing $80 billion in stock losses, demonstrate both the government's regulatory reach and its sensitivity to market reactions.

Monetization models in China emphasize social interaction and community building over individual progression. The most successful games integrate social features, guild systems, and community events that align with Chinese cultural preferences for collective achievement. Tencent's Honor of Kings exemplifies this approach, generating over $1 billion through social monetization rather than pay-to-win mechanics.

Anti-addiction measures for minors limit gaming to one hour on weekdays and two hours on weekends, with complete restrictions between 10 PM and 8 AM. These regulations have fundamentally altered game design, pushing developers toward shorter session lengths and social rather than progression-based engagement.

Japan: Console Heritage Meets Mobile Innovation

Japan's $6.19 billion gaming market represents a unique blend of traditional console gaming heritage and innovative mobile experiences. Home to Nintendo, Sony PlayStation, and countless influential franchises, Japan maintains strong console and PC gaming segments despite mobile's growth to represent the largest platform by revenue.

Japanese gaming culture emphasizes quality, polish, and attention to detail that extends far beyond graphics to include user experience, narrative depth, and cultural authenticity. Games like Genshin Impact succeed not just through technical excellence but by incorporating anime aesthetics, Japanese voice acting, and storytelling conventions that resonate with local audiences.

The domestic gaming industry continues to influence global trends despite increased international competition. Nintendo's hybrid console strategy with the Switch has redefined portable gaming, while Sony's PlayStation 5 maintains premium positioning in the console market. Japanese developers like FromSoftware (Elden Ring), Square Enix (Final Fantasy), and Capcom (Monster Hunter) consistently produce globally successful titles that begin with deep Japanese market understanding.

Mobile gaming monetization in Japan pioneered the gacha model that has spread worldwide. Japanese players demonstrate sophisticated understanding of gacha mechanics and higher tolerance for these systems when implemented with cultural sensitivity around fairness, transparency, and value proposition. The average revenue per user (ARPU) in Japanese mobile gaming exceeds most global markets, reflecting both higher disposable income and cultural acceptance of gaming expenditure.

Japanese game development emphasizes iterative polish and long-term content strategies. Unlike markets focused on rapid launch cycles, Japanese developers often spend years perfecting games before release, then support them with consistent updates for extended periods. This approach creates deeper player engagement and higher lifetime values, but requires significant upfront investment and patient capital.

The distribution landscape includes both international platforms and strong domestic alternatives. While iOS App Store and Google Play maintain significant presence, platforms like DMM Games, GREE, and Mobage serve specific audience segments with different content preferences and monetization approaches. Success often requires understanding which platform best serves your target demographic within the broader Japanese market.

Localization requirements extend beyond language to include cultural adaptation of characters, narratives, and game mechanics. Japanese players expect deep customization options, sophisticated progression systems, and integration with popular cultural franchises. Voice acting quality particularly matters, with many players preferring Japanese voice work even for international games.

The anime and manga integration represents a unique opportunity within Japanese gaming. Games that successfully incorporate popular franchises, character archetypes, and narrative structures from anime culture often achieve breakout success. However, this requires authentic understanding rather than superficial adaptation of anime aesthetics.

Platform distribution differs significantly from other markets, with strong domestic app stores and gaming platforms complementing international options. Partnerships with local distributors like DeNA, GREE, or CyberAgent often prove essential for market access and cultural credibility, particularly for companies lacking established Japanese market presence.

South Korea: eSports and Innovation Leadership

South Korea's $5.78 billion gaming market has global influence far exceeding its size, driven by advanced infrastructure, competitive gaming culture, and technological innovation. With 52 million people and near-universal high-speed internet access, Korea represents the world's most connected gaming environment.

eSports culture permeates Korean gaming in ways that other markets struggle to replicate. Professional gaming enjoys mainstream recognition, with players achieving celebrity status and tournaments drawing massive audiences. This competitive culture influences game design preferences toward skill-based mechanics, balanced gameplay, and spectator-friendly features. The success of games like League of Legends, StarCraft, and locally developed titles demonstrates how competitive balance and skill ceiling affect long-term player engagement.

PC gaming maintains stronger market share in Korea than most Asian markets, driven by PC bang (internet cafe) culture and competitive gaming preferences. While PC bangs have evolved from necessity to social gaming spaces, they continue to influence game preferences toward titles that support social play, competitive interaction, and extended gaming sessions. The PC bang ecosystem also affects monetization, with many games offering PC bang-specific benefits and hour-based pricing models.

Korean gaming companies have developed technological innovations that influence global gaming development. NCSoft's Lineage franchise pioneered many MMORPG mechanics, Nexon developed free-to-play monetization models that spread globally, and Netmarble has created cross-platform systems that other developers study. These companies often serve as testing grounds for monetization strategies and technical innovations that later spread to other markets.

The regulatory environment creates unique challenges around gambling mechanics and speculative content. Korea's interpretation of gambling laws affects game design more restrictively than most markets, with even loot box mechanics facing increased scrutiny. Recent court decisions supporting government restrictions on blockchain games signal continued regulatory caution around any content that could be construed as speculative or gambling-related.

Mobile gaming adoption in Korea reflects sophisticated user preferences and high technical standards. Korean mobile gamers expect console-quality experiences, advanced social features, and seamless cross-platform functionality. The success of games like PUBG Mobile and various battle royale titles demonstrates Korean players' preference for competitive, skill-based mobile experiences rather than casual gaming.

The Korean gaming industry's global export success provides valuable lessons for international market development. Companies like Krafton (PUBG), Pearl Abyss (Black Desert), and Smilegate (CrossFire) have achieved global success by combining Korean game development expertise with international market understanding. Their approaches to localization, community building, and live service operations offer blueprints for other companies seeking global expansion.

Social integration in Korean games reflects broader cultural preferences for community interaction and competitive achievement. Features like guild systems, ranking displays, and social sharing integrate deeply with Korean social media and communication platforms. Understanding these social dynamics proves essential for both game design and marketing strategy within the Korean market.

However, Korea's regulatory environment creates unique challenges. Online gambling restrictions are among the world's strictest, and even games with perceived gambling mechanics face regulatory scrutiny. The recent court decisions supporting government restrictions on blockchain games signal continued regulatory caution around speculative gaming elements.

Southeast Asia: Mobile-First Growth Engine

Southeast Asia's gaming market represents the fastest-growing segment in Asia Pacific, with revenue increasing 53.2% year-over-year in 2024 following a post-pandemic recovery. The SEA-6 markets—Indonesia, Malaysia, Philippines, Singapore, Thailand, and Vietnam—will host 332 million gamers by 2028, equivalent to the current U.S. population.

Mobile gaming dominates with over 70% of revenue, driven by smartphone penetration reaching 78% in 2023 and projected to hit 90% by 2030. Unlike mature markets where mobile gaming evolved from existing platforms, Southeast Asia built mobile-first gaming ecosystems that bypass traditional console and PC gaming entirely. This creates unique opportunities for companies that understand mobile-native game design and monetization.

Indonesia leads the region with 41% of total downloads and represents the largest single market by user base. With over 270 million people and rapidly growing internet infrastructure, Indonesia offers massive scale but requires understanding of diverse cultural and economic segments across thousands of islands. Local payment methods like Dana and OVO are essential for market penetration, while content must be adapted for both urban and rural Indonesian preferences.

Thailand emerges as the revenue leader despite smaller population, generating over $400 million in mobile gaming revenue in 2024. Thai players demonstrate higher spending patterns and engagement levels, making Thailand particularly attractive for premium mobile gaming experiences. The Thai market also shows strong eSports engagement and responds well to competitive gaming features.

Vietnam represents the fastest-growing market within SEA-6, with gaming time increasing most dramatically in 2024. Vietnamese players show particular interest in RPG and strategy games, with local developers like VNG creating culturally relevant content that competes successfully with international titles. The Vietnamese market requires careful attention to local payment preferences and government content guidelines.

The Philippines stands out for its English proficiency and cultural connections to Western gaming preferences, while maintaining distinct local characteristics. Filipino players demonstrate strong social gaming preferences and community engagement, making the Philippines an ideal testing ground for social features and community-driven monetization strategies.

Singapore and Malaysia represent more mature markets within SEA-6, with higher per-capita spending and sophisticated user preferences. These markets often serve as entry points for international companies due to English proficiency and familiar business environments, but success requires understanding that high-income markets demand premium experiences.

Cultural and linguistic diversity creates both opportunities and challenges. Over 1,000 languages are spoken across the region, with successful games requiring localization for Indonesian, Thai, Vietnamese, and other major languages. Cultural preferences vary significantly, with Indonesian players favoring different social features than Vietnamese users, even within the same game.

Payment systems reflect regional financial infrastructure, with digital wallets used by over 75% of gamers. Traditional banking penetration varies widely, making alternative payment methods essential for market access. Thai players prefer different payment systems than Filipino users, requiring flexible payment integration strategies that accommodate local financial ecosystems.

eSports engagement exceeds 50% of gamers across SEA-6 markets, with mobile eSports tournaments driving both participation and viewership. Games like Mobile Legends: Bang Bang and Garena Free Fire achieve success through community building and competitive gaming features rather than traditional progression mechanics. The eSports ecosystem in Southeast Asia is increasingly professionalized, with government support and corporate sponsorship creating sustainable competitive gaming opportunities.

Female gamers represent significant purchasing power, with 30% of women making game-related purchases compared to 22% of men. This demographic requires inclusive game design, meaningful female character representation, and harassment protection systems that many international games overlook. Companies that successfully engage female gamers in Southeast Asia often achieve higher lifetime values and stronger community engagement.

Local game development is emerging as a significant trend, with titles like Coral Island (Indonesia), GigaBash (Malaysia), Cat Quest (Singapore), and Home Sweet Home: Online (Thailand) achieving both regional and international success. These locally developed games demonstrate understanding of regional preferences and cultural nuances that international developers often miss.

Government support varies significantly across SEA markets. Singapore offers tax incentives and incubator programs for gaming companies, Malaysia's DICE policy attracts foreign investment, while Indonesia's AGI organization promotes local industry development. Understanding government priorities and available incentives can significantly impact market entry costs and long-term sustainability.

India: The Fastest-Growing Frontier

India's gaming market, valued at $4.04 billion in 2025 and projected to reach $8.36 billion by 2030, represents the world's fastest-growing major gaming economy. With 568 million gamers and 680 million smartphone users, India combines massive scale with explosive growth rates that exceed all other major markets. The sheer demographic advantage—with over 600 million people under age 35—creates a gaming audience larger than the entire population of North America.

Mobile gaming dominates with 80% of market revenue, supported by the world's most affordable data costs at $0.26 per gigabyte compared to $6.66 in the UK and $12.37 in the US. This infrastructure advantage enables gaming experiences that would be cost-prohibitive in other emerging markets, while also creating opportunities for data-heavy games that might struggle elsewhere due to cost constraints.

The diversity of Indian markets requires sophisticated segmentation strategies. Tier 1 cities like Mumbai, Delhi, and Bangalore demonstrate gaming preferences similar to international markets, while Tier 2 and Tier 3 cities show distinct preferences for localized content, regional language support, and culturally relevant gameplay mechanics. Successful companies often develop different engagement strategies for urban and rural segments.

Localization requirements extend beyond the 22 official languages to include cultural adaptation for diverse regional preferences. Hindi, English, Tamil, Telugu, and Bengali represent primary languages, but successful games also consider regional cultural differences in gameplay preferences, social features, and monetization approaches. The complexity of Indian localization often surprises international companies accustomed to single-language markets.

The Indian gaming industry benefits from strong domestic development capabilities. Companies like Dream 11, Game24X7, and Mobile Premiere League have achieved unicorn status by understanding local preferences and regulatory requirements. These companies demonstrate how India-first development can create globally relevant products while serving local market needs.

Government support through initiatives like the Animation, Visual Effects, Gaming, and Comics (AVGC) Promotion Task Force and Digital Games Tax Offset creates favorable business conditions. The gaming industry is projected to generate 250,000 jobs over the next decade, supplementing the existing 100,000 direct and indirect employees. This government support includes training programs, regulatory frameworks, and tax incentives that reduce barriers to entry for both domestic and international companies.

eSports growth has been remarkable, with recognition as a legitimate sport and integration into multi-sport events. The establishment of proper eSports infrastructure, tournament organizing bodies, and professional leagues creates opportunities for both competitive gaming and related services. Indian eSports particularly succeeds in mobile gaming categories, reflecting the broader mobile-first nature of the market.

Payment integration requires understanding India's unique digital payment ecosystem, including UPI (Unified Payments Interface), digital wallets like Paytm and PhonePe, and prepaid gaming cards. The success of digital payments in India—often exceeding adoption rates in developed markets—creates opportunities for seamless in-game monetization when properly integrated with local payment preferences.

The rise of disposable income among India's middle class, projected to reach INR 305 million in 2024, drives increased gaming spending and in-app purchase adoption. However, pricing strategies must reflect local economic conditions, with successful games often employing value-based pricing that provides significant content at lower price points than international standards.

Content preferences in India span traditional games like Teen Patti and Rummy alongside international genres like battle royale and RPGs. However, the most successful games incorporate Indian cultural elements, mythology, or social dynamics that resonate with local players. Games featuring Indian festivals, cultural celebrations, or familiar social structures often achieve higher engagement than direct imports of international titles.

The regulatory environment continues evolving, with recent guidelines from the National Law University Delhi and E-Gaming Federation establishing frameworks for legitimate gaming operations. These regulations aim to distinguish skill-based gaming from gambling while protecting consumers and promoting industry growth. Understanding these regulatory distinctions proves essential for long-term market success.

Australia and New Zealand: Mature Western Markets

Australia's $2.5 billion gaming market and New Zealand's $420 million presence represent mature, Western-style gaming ecosystems within the Asia Pacific region. These markets provide familiar regulatory environments and cultural preferences for Western companies expanding into Asia, often serving as testing grounds for broader Asian market strategies.

Australia's gaming industry benefits from government support through the Digital Games Tax Offset (DGTO), allowing studios to claim 30% of eligible expenditures, with additional state-based incentives reaching 10-15%. This support has helped local development flourish while attracting international investment, creating a vibrant ecosystem of both local and international studios. The success of Australian developers like Team Cherry (Hollow Knight) and House House (Untitled Goose Game) demonstrates the creative potential within this supportive environment.

Console gaming maintains stronger market share than in most Asian markets, with PlayStation, Xbox, and Nintendo representing significant revenue streams. Australian gamers demonstrate purchasing patterns similar to North American markets, with strong preference for premium games, downloadable content, and gaming hardware. The console gaming market reached $419.84 million in 2024, showing continued growth despite mobile gaming expansion.

PC gaming also remains viable, supported by strong broadband infrastructure and gaming community culture. The Australian PC gaming market benefits from high-quality internet infrastructure and a tech-savvy population comfortable with digital distribution platforms like Steam, Epic Games Store, and local alternatives.

Mobile gaming growth follows global patterns rather than the mobile-first adoption seen in other Asian markets. Australian mobile gamers expect console-quality experiences adapted for mobile platforms, rather than mobile-native game designs. This creates opportunities for companies that can successfully adapt premium gaming experiences for mobile platforms while maintaining quality expectations.

The Australian gaming demographic skews older than many Asian markets, with significant gaming populations in the 25-44 age range representing peak earning years. This demographic demonstrates higher spending power and willingness to purchase premium gaming experiences, DLC, and gaming hardware. Understanding these demographic preferences proves essential for monetization strategy and marketing approaches.

Distribution strategies in Australia and New Zealand closely resemble Western markets, with strong retail presence complementing digital distribution. Major retailers like EB Games, JB Hi-Fi, and Big W continue to play important roles in hardware sales and game discovery, while digital platforms dominate software sales.

Regulatory frameworks in both countries follow Western models with self-regulation through industry bodies like the Interactive Games and Entertainment Association (IGEA). Content classification through the Australian Classification Board follows familiar rating systems, making market entry straightforward for companies experienced in Western markets. However, Australia's strict content guidelines around certain themes require attention during localization.

The Australian and New Zealand markets also serve as valuable entry points for understanding broader Asian market dynamics while operating in familiar regulatory and cultural environments. Many international companies use these markets to test Asian expansion strategies, build regional expertise, and establish operational infrastructure before expanding into more complex Asian markets.

eSports adoption in Australia follows Western patterns with strong engagement in traditional PC and console competitive games. The Australian eSports scene, while smaller than Asian powerhouses, demonstrates sophistication and infrastructure development that influences broader gaming market development.

Emerging Markets and Secondary Opportunities

Beyond the major Asian gaming markets, several emerging economies present significant opportunities for forward-thinking companies. These markets often require different approaches than established territories but offer first-mover advantages and higher growth potential for companies willing to invest in long-term market development.

Taiwan represents a sophisticated gaming market with strong mobile and PC gaming adoption. Taiwanese players demonstrate preferences similar to mainland China but operate under different regulatory frameworks that allow greater content freedom. The market serves as a valuable testing ground for Chinese market strategies while providing revenue opportunities in its own right.

Hong Kong maintains its position as a regional gaming hub despite its smaller size, with sophisticated players and strong spending power. The market's international orientation and English proficiency make it accessible for Western companies, while its cultural connections to mainland China provide insights for broader Chinese market strategies.

Bangladesh, Pakistan, and Sri Lanka represent frontier markets with massive demographic potential but significant infrastructure and regulatory challenges. These markets require patient capital and local partnership strategies, but offer opportunities for companies that can navigate the complexity. Mobile-first strategies prove essential given limited traditional gaming infrastructure.

The Pacific Island markets, including Fiji, Papua New Guinea, and various smaller territories, represent niche opportunities with unique cultural characteristics and growing internet penetration. While these markets are small individually, they can provide valuable insights into underserved gaming demographics and serve as testing grounds for innovative approaches to market development in challenging environments.

Regulatory Landscapes and Market Access

Regulatory complexity varies dramatically across Asian markets, creating both barriers and opportunities for international companies. China's comprehensive approval process represents the most stringent requirements, while markets like Singapore and Australia operate under more familiar Western-style regulatory frameworks.

Content restrictions differ significantly between markets. While China prohibits content deemed contrary to national values, Korea restricts gambling-related mechanics, and India requires compliance with local cultural sensitivities. Japan's content regulations focus more on disclosure requirements for monetization mechanics than content censorship.

Age verification and minor protection systems require different approaches across markets. China's comprehensive anti-addiction systems mandate specific technical implementations, while other markets rely more on industry self-regulation and parental controls.

Data localization requirements create technical and compliance challenges. China requires domestic data storage for user information, while other markets have varying requirements around data sovereignty and privacy protection. Understanding these requirements early in development prevents costly technical retrofitting.

Tax and revenue sharing structures vary significantly, with some markets offering development incentives while others impose significant revenue-sharing requirements. Australia's tax offsets contrast sharply with markets that require local publishing partnerships and revenue sharing arrangements.

Cultural Considerations and Localization

Cultural adaptation extends far beyond language translation to encompass gameplay mechanics, social features, and monetization approaches. Japanese players expect deep customization and progression systems, while Southeast Asian markets prioritize social interaction and community features.

Character design and narrative elements require cultural sensitivity. Anime-inspired aesthetics succeed in Japan and certain Southeast Asian markets but may not resonate in India or Australia. Historical themes popular in China and Korea may be inappropriate or irrelevant in other markets.

Social features must align with cultural communication patterns. Chinese players prefer guild-based social systems, Korean players value competitive rankings, and Southeast Asian markets emphasize casual social interaction. These preferences influence both game design and marketing strategies.

Monetization psychology differs significantly between cultures. Japanese players accept gacha mechanics when implemented transparently, Chinese players prefer social monetization over individual advancement, and Indian players respond to value-based pricing that reflects local economic conditions.

Technology Infrastructure and Platform Preferences

Technology infrastructure varies dramatically across Asian markets, influencing platform preferences and technical requirements. Korea and Japan maintain advanced broadband and 5G networks that support sophisticated gaming experiences, while emerging markets in Southeast Asia and India require optimization for lower-bandwidth environments.

Platform preferences reflect both infrastructure and cultural factors. PC gaming remains strong in Korea due to PC bang culture, console gaming maintains relevance in Japan through cultural heritage, and mobile gaming dominates in markets with limited traditional gaming infrastructure.

Cloud gaming adoption varies based on infrastructure quality and cultural acceptance. Advanced markets like Korea and Japan show strong cloud gaming potential, while emerging markets may leapfrog traditional platforms entirely as infrastructure improves.

Payment infrastructure differences require flexible integration strategies. While China operates primarily through WeChat Pay and Alipay, Southeast Asian markets use diverse digital wallet systems, and traditional markets like Australia and New Zealand require conventional payment processing.

Future Trends and Strategic Implications

Asia Pacific gaming markets are converging around several key trends while maintaining distinct characteristics. Mobile gaming continues expanding across all markets, but implementation varies based on cultural preferences and infrastructure capabilities.

Cross-platform gaming gains importance as players expect seamless experiences across devices. This trend favors companies that can provide consistent experiences while adapting to local platform preferences and technical constraints.

eSports integration becomes table stakes rather than competitive advantage, with successful games building competitive features from launch rather than adding them later. However, eSports implementation must reflect local competitive cultures and viewing preferences.

Regulatory evolution continues across all markets, generally toward greater oversight and consumer protection. Companies that proactively implement responsible gaming features and transparent monetization will be better positioned for long-term success.

AI and machine learning adoption varies by market sophistication and regulatory environment. Advanced markets embrace AI for personalization and content generation, while emerging markets focus on AI applications that improve accessibility and reduce technical barriers.

Strategic Recommendations for Market Entry

Successful Asian market entry requires rejecting one-size-fits-all approaches in favor of market-specific strategies. Companies should prioritize understanding regulatory requirements, cultural preferences, and technical constraints before developing localization strategies.

Partnership strategies vary by market maturity and regulatory requirements. China and Korea often require local publishing partnerships, while mature markets like Australia and Japan allow direct market entry with appropriate localization.

Investment in local teams provides cultural intelligence that remote operations cannot replicate. The most successful international companies build local expertise rather than imposing external approaches on unfamiliar markets.

Phased market entry allows testing and iteration before full commitment. Starting with markets that match existing capabilities while building expertise for more complex markets reduces risk and improves long-term success probability.

Asia Pacific represents the world's largest gaming opportunity, but success requires sophisticated understanding of market differences, cultural nuances, and regulatory complexities. Companies that invest in this understanding will capture disproportionate value in the world's most dynamic gaming ecosystem.

Navigating Asia's complex gaming markets requires deep regional expertise and cultural intelligence. At RedKing Marketing, we help international gaming companies develop market-specific strategies that unlock sustainable growth across Asian markets. Contact us to build your Asian gaming market strategy with confidence.